From Concrete to Carbon Neutral: Decarbonizing Asia’s Built Environment

November 5, 2024

This whitepaper is a joint initiative between BCG X, B Capital, and Accacia.

Introduction

The Sixth Assessment Report from the United Nations Intergovernmental Panel on Climate Change underscores the critical role of the real estate sector in addressing global warming. Buildings account for roughly 40% of global carbon emissions, with 29% arising from daily energy consumption and 11% from construction activities. Improving building energy efficiency and lowering carbon footprints are essential steps in mitigating climate change.

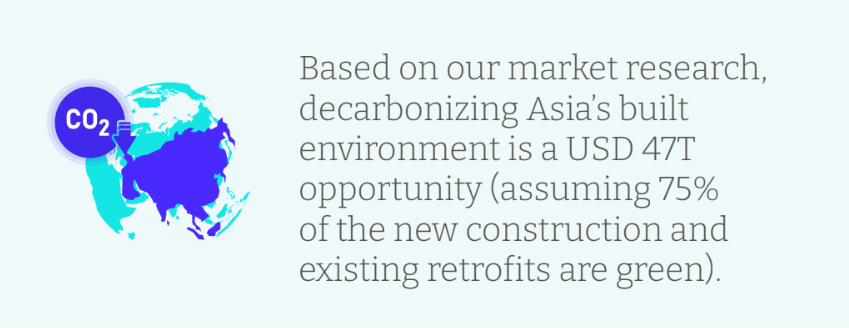

Asia is at the forefront of this climate change crisis. According to the World Economic Forum, the region accounts for around 50% of global emissions—a figure that is expected to rise in parallel with ongoing construction activities. While Asia already comprises about 50% of the global real estate market today, it is expected to add over 70 billion square meters of real estate in the next two decades.

Decarbonizing Asia’s built environment will require a multifaceted approach, focusing on sustainable urban planning, innovation in construction materials, optimizing operations and retrofitting existing buildings for better energy efficiency.

Outlined below are four key levers to decarbonize Asia’s built environment.

01 The Key Decarbonization Levers in Asia

1. Limiting Urban Sprawl

As hubs of economic activity, cities emit over 70% of global CO2. With more than half of the world’s urban population, Asian cities are responsible for a significant share of these emissions. A carbon footprint mapping exercise of 13,000 cities conducted by NASA[1] revealed that seven of the top 10 emitters and 10 of the top 10 per capita emitters are in Asia, underscoring the imperative for Asian cities to adopt sustainable urban development practices.

Urban sprawl, characterized by low-density development, inherently demands more transportation infrastructure and energy, leading to significantly higher emissions. Studies have shown that the rate of urban land expansion in China has outpaced population growth[2], exacerbating urban sprawl and its associated environmental impacts. To counter this, cities need to be planned to limit sprawl and create multi-use high-intensity zones.

2. Decarbonizing the Construction Process

Embodied carbon, which can constitute up to 50% of a building’s total lifetime emissions, is largely determined by material choice and procurement processes.

In Asia, the material manufacturing sector can be fragmented, with multiple suppliers contributing raw materials and components to the production process. Project developers often hesitate to adopt lower-carbon materials due to their higher upfront costs and a perception that these alternatives lack the quality and durability of traditional materials like cement, iron, steel, and aluminum, which are notably carbon-intensive.

There are some promising technologies in this space, but it will take time for them to be widely adopted.

Case Study

Building Tomorrow:

Lodha

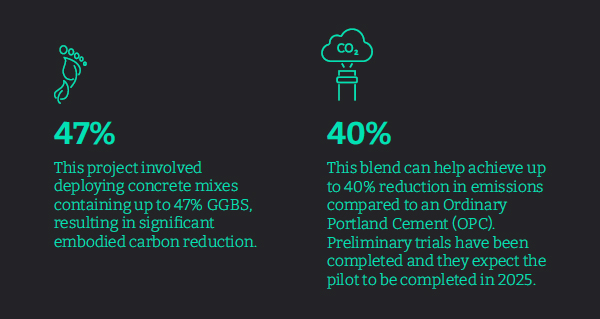

Lodha, a leading real estate developer in India, has been at the forefront of sustainable building practices. Given that concrete is one of the most carbon-intensive building materials, they have been innovating to develop greener concrete mixes.In a pilot project, Lodha explored using GGBS (a steel industry by-product) as a low-carbon alternative and supplementary cementitious materials (SCM) in concrete for high-rise construction.

Despite the benefits, the use of GGBS and other SCMs in construction face several challenges, such as delayed strength gain and issues with pumpability at greater heights. Nevertheless, the enhanced durability and performance of these materials encourages their adoption in

superstructure construction.

Lodha has also partnered with IIT Delhi for the pilot use of an innovative blend, LC3 (limestone calcined clay cement).

Case Study

Building Tomorrow:

ceEntek

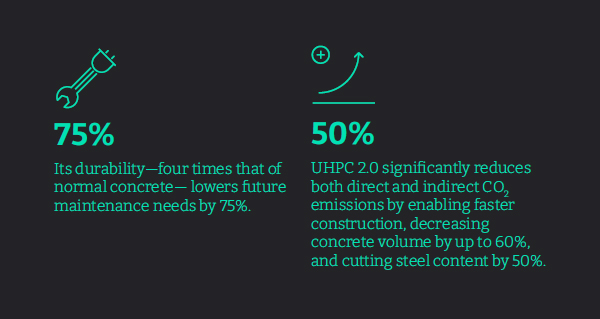

ceEntek, a leader in advanced Ultra-High Performance Concrete (UHPC) technologies, was founded in Singapore in 2010. The company is transforming the concrete industry with its UHPC 2.0™ product, incorporating carbon nanofibers (CNF) to enhance mechanical and durability properties. This innovation addresses the challenges of traditional UHPC, such as complex production processes and high costs, by simplifying the ingredients to five essential components: cement, sand, water, CNF, and a plasticizer.The material’s high strength and rapid early strength development accelerate construction, reducing the typical 28-day curing period to just a few days. For instance, in a recent bridge construction project using CeEntek’s UHPC 2.0™, CO2 emissions were reduced from 124,080 kg with traditional materials to only 41,675 kg.

3. Implementing Carbon Capture, Utilization, and Storage Solutions

Broader carbon capture and storage technologies also present significant opportunities for emissions reduction. Implementing Carbon Capture, Utilization, and Storage (CCUS) technologies—such as chemical absorption and calcium looping—offers effective methods to decrease emissions from material production.

CCUS technologies, along with negative emission technologies aimed at directly removing carbon from the atmosphere, are still in early development stages and face significant technological barriers.

However, innovative projects are reshaping the industry. For example, a house in Karuizawa, Japan was recently constructed using the world’s first CO2-removing concrete, CO2-SUICOM[3]. Despite these advancements, scaling these innovations to commercial viability requires significant capital investment.

4. Advancing the Use of Data and Artificial Intelligence

Without standardized frameworks for conducting Life Cycle Assessments (LCA) or mandates for reporting akin to Environmental Product Declarations (EPD) seen in the EU and US, transparency remains low for production processes in Asia. To date, fewer than 10,000 of the global 100,000 EPD declarations originate from Asia.

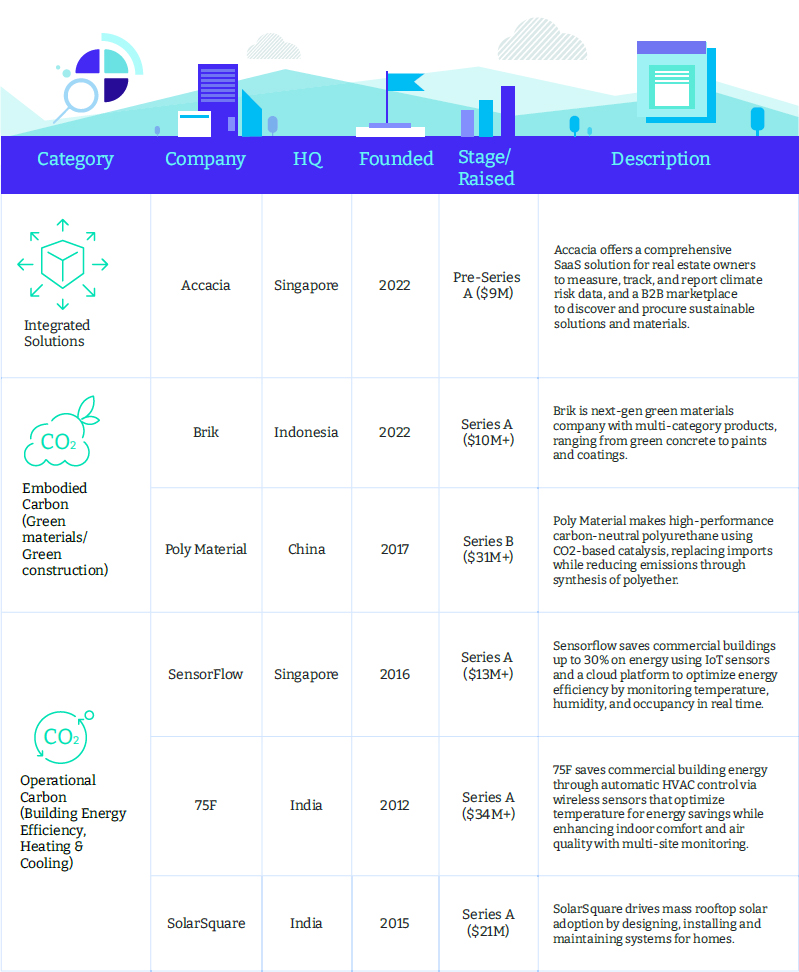

Startups are emerging as pivotal players in organizing data flow and increasing supply chain transparency. Innovative platforms like Accacia are enabling materials manufacturers in Asia to perform lifecycle assessments and generate EPDs. Accacia has enabled manufacturers across 25+ categories of construction materials to generate EPDs and recently assisted a $100bn+ AUM real estate asset manager to incorporate Greenhouse Warming Potential (GWP) as a key metric in their tendering process.

Case Study

Data Collection and Tracking:

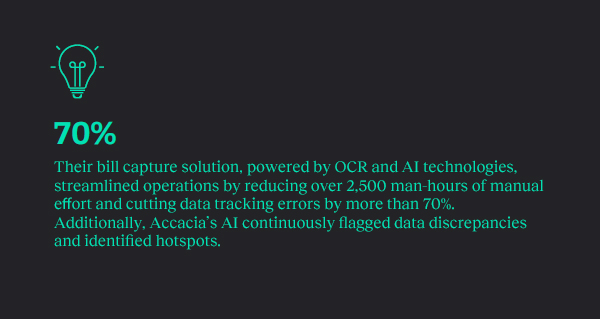

Accacia

Accacia deployed its SaaS solution with an Asia-based financial services company to address the substantial challenge of tracking emissions across more than 2,000 physical locations in the region.By integrating Utility Bills, Smart Meters and Building Management Systems (BMS), asset owners can capture more granular energy consumption data, enabling real-time tracking, automated preventive maintenance and a reduction in energy-related emissions.

02 Putting Capital to Work in Asia to Address the Opportunity

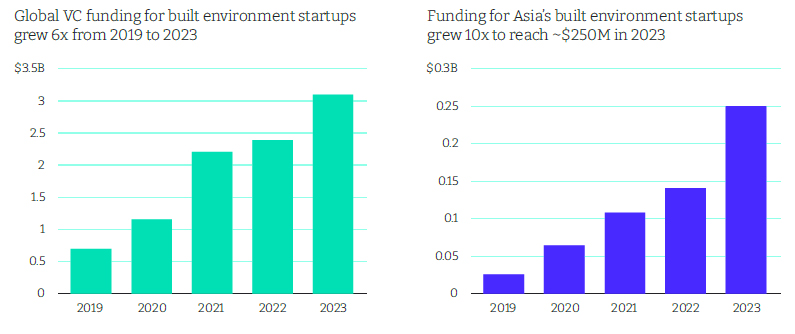

The VC industry has been actively investing in innovation across the built environment. Despite significant global growth in built environment start-up funding, Asia has yet to claim its fair share.

In 2023, venture capital investments in this sector surpassed $3 Billion globally, but Asian startups secured only 10% of this funding.

Asia’s built environment funding grew 10x from 2019 to 2023 but still remains only 10% of total global funding

Notes: VC funding (Seed to pre-IPO) considered; Doesn’t include PE, IPO, Buyouts, M&A, Grants, Corporate Deals

Source: Pitchbook, Secondary Research

We see this trend changing in the next 10 years with the emergence of climate focused funds and game-changing climate technologies being built in Asia.

Source: Pitchbook, Secondary Research

Corporates and financial institutions in Asia also have a role to play and must take the lead in strategically allocating capital towards sustainable industries and practices. Corporates, as major contributors to greenhouse gas emissions, carry a significant responsibility in driving change. They must not only invest financially but also dedicate their time, expertise, and resources to actively seek out and pilot innovations that can transform their sectors. By leveraging their scale and influence, corporates can accelerate the adoption of sustainable technologies, creating a ripple effect throughout their supply chains and industries. This dual approach—combining financial investment with active engagement in innovation—is crucial for corporates to shift from being part of the problem to becoming instrumental in the solution, ultimately driving meaningful progress in the fight against climate change.

Singapore stands at the forefront of sustainability innovations, marked by a surge in investments and innovation efforts aimed at the green economy. Companies are also increasingly recognising corporate venturing – which includes both corporate venture creation and startup partnerships – as a powerful tool in their innovation strategy. The third edition of the Corporate Venture Launchpad (CVL) programme has been expanded to support companies in developing sustained venture creation capabilities as well as establishing best practices for effective corporate-startup collaborations, leading to impactful business outcomes.

Corporate venturing is vital for Singapore’s green economy as it enables the rapid scaling of innovative sustainability solutions, reduces time-to-market for green technologies, and aligns with the nation’s broader goals of environmental stewardship and economic resilience. These corporate venturing efforts allow Singapore to position itself at the forefront of global sustainability efforts while simultaneously driving economic growth and securing a greener future.

~ Mr. Yuan Chun Ling, Vice

President of EDB

Case Study

Sustainability X Challenge:

CapitaLand

CapitaLand Group, a leading diversified real estate group in Asia, is at the forefront of driving innovation to address climate risks in real estate. It launched the CapitaLand Sustainability X Challenge (CSXC), a global platform seeking sustainable solutions for the built environment. CapitaLand closely collaborates with industry partners and government agencies like Singapore’s Building and Construction Authority (BCA) and Enterprise Singapore (EnterpriseSG), as well as experts from academia, in reviewing submissions and mentoring innovators.CSXC gives innovators the opportunity to broaden their reach through introductions to CapitaLand partners. The annual challenge culminates in a Demo Day, which saw 350 in-person and 1,000 virtual attendees in 2023.

After the Demo Day, CapitaLand works extensively with the innovators to customise their piloting protocol plan, a process that is new to many of them. Finally, unlike most innovation challenges, CSXC provides the opportunity to pilot innovations within a live asset which provides data verification, lessons learned, as well as compelling case studies upon successful completion of the pilot.

Conclusion

Decarbonizing Asia’s built environment presents a critical opportunity to mitigate climate change while addressing the region’s rapid urbanization. Buildings, which account for nearly 40% of global carbon emissions, are central to achieving this goal, especially given Asia’s significant share of current and future construction. The strategies outlined in this report, such as limiting urban sprawl, decarbonizing construction processes, and leveraging technologies like carbon capture and artificial intelligence, are pivotal in reducing emissions.

Investment in climate-focused ventures, as well as corporate engagement in pilot projects and innovation partnerships, are key drivers in accelerating the decarbonization process. By integrating these approaches, Asia’s built environment can transform into a more sustainable model, ensuring economic growth aligns with environmental stewardship.

About the authors

Karan Mohla, General Partner, B Capital

Karl Noronha, Vice-President, Strategy & Operations, B Capital

Mehul Garg, Associate, B Capital

Annu Talreja, Founder & CEO, Accacia

Piyush Chitkara, Co-founder & CTO, Accacia

Hanno Stegmann, Managing Director & Partner, BCGX

Neels Steyn, Partner, BCGX

Megha Kehar, Lead Product Manager, BCGX

Amar Sood, Independent Researcher

Avinash Jain, Sr. Business Analyst, Accacia

[1] Voiland, A.,(2019), ‘Sizing Up the Carbon Footprint of Cities’. Available at: Link Here [14 July 2024]

[2] Wang, Y., Chunlin H., Yaya F., Minyan Z., and Juan G., 2020, “Using Earth Observation for Monitoring SDG 11.3.1-Ratio of Land Consumption Rate to Population Growth Rate in Mainland China” Remote Sensing 12, no. 3: 357. Link here [16 July 2024].

[3] CO2-SUICOM, standing for CO2-Storage and Utilization for Infrastructure by Concrete Materials, was used in a house designed by Nendo, a Japanese design studio.